How to Decide Between Faster Debt Payoff and Emergency Savings

Frank's hands were rough, his back was sore, and his boots were dusty by 5 p.m. every day. But what really weighed on him was the $9,000 in credit card debt hanging over his head like a scaffold ready to fall.

He had about $600 a month he could put toward a debt payoff plan. That sounds simple until you hit the real question: should you throw every extra dollar at debt, or should you build savings at the same time?

One guy said, "Put it all on the card and get rid of it." Another guy said, "Save some of it. You never know when your truck's going to quit."

Frank was not just trying to get out of debt. He was trying to avoid ending up right back in it.

Two Debt Payoff Plans - Which One Works Best?

This is where a lot of people get stuck. A fast payoff plan feels smart because the debt disappears sooner. A balanced plan feels slower, but it can protect you from having to start over if real life hits before the cards are gone.

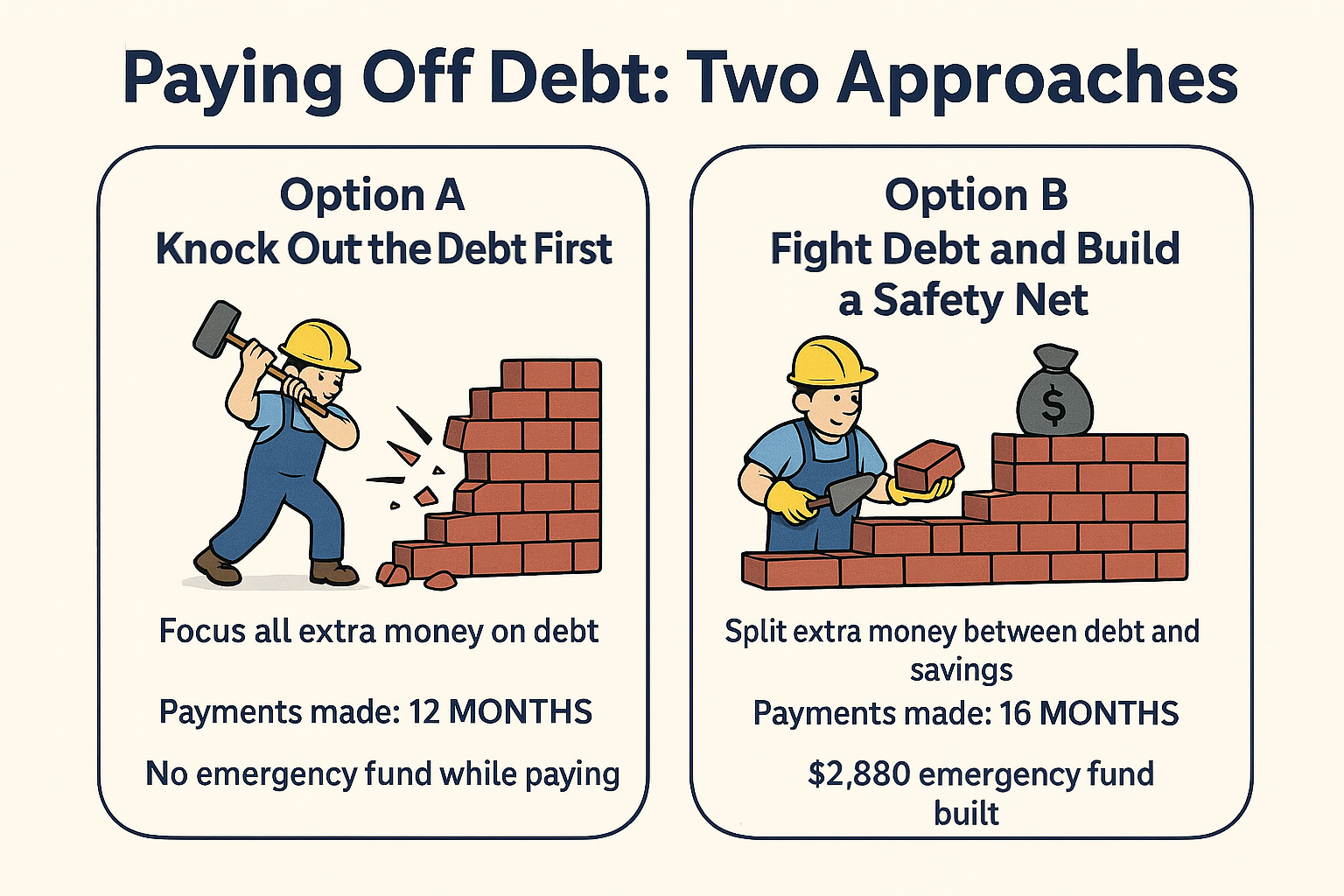

Plan A: Pay Off Debt as Fast as Possible

Frank could throw the full $600 extra at the cards every month. Add that to his regular $240 minimum payment, and he would be paying $840 a month total.

That would wipe out the full $9,000 in about 12 months.

Upside: The debt is gone faster.

Risk: If the truck breaks down, tools need replacing, or work slows down, he has no safety cushion and may need to use credit again.

Fast, yes. But exposed.

Plan B: Pay Off Debt While Building Savings

Frank could put $420 extra toward the card and place $180 a month into emergency savings.

That means the debt takes about 16 months instead of 12, but he also builds about $2,880 in savings.

Upside: He still makes steady progress and builds a financial buffer at the same time.

Tradeoff: It takes longer than the all-out payoff plan.

Slower, yes. But sturdier.

This is why the right debt payoff plan is not always the fastest one on paper. If you focus only on debt, you can leave yourself exposed. If you focus only on savings, interest keeps chewing away at your progress. In many real-world cases, a balanced plan gives you the best shot at making progress and keeping it.

Why the Balanced Plan Made More Sense

Frank chose Plan B because it matched the way real life works. He did not want a debt strategy that looked great until the first surprise expense showed up.

He knew something many people learn the hard way: paying off debt too aggressively can backfire when you have no backup plan. One repair bill, one bad month, or one emergency can put you right back where you started.

So instead of chasing the fastest possible finish, he chose a debt payoff plan that gave him two things at once: progress and protection.

Should You Pay Off Debt Fast or Build Savings First?

If you are trying to decide, ask yourself one honest question:

or slower and protected?

There is no universal answer for everyone. But if you have no emergency cushion at all, splitting your extra money between debt payoff and savings may be the smarter move.

That is especially true if your life has any volatility at all - irregular income, old vehicles, kids, seasonal expenses, surprise repairs, or a job situation that is not perfectly predictable.

🚨 What Happens If You Do Nothing?

- $9,000 can turn into far more over time because interest keeps working against you.

- One bad week or one repair bill can push you deeper into debt.

- Without savings, even a small emergency can undo months of progress.

- The longer you wait, the more money disappears into interest instead of helping you move forward.

What This Means for Your Own Debt Payoff Plan

If this story sounds familiar, the next step is not guessing harder. The next step is running the numbers and seeing what your own tradeoff looks like.

A good debt payoff tool helps you compare options, see your payoff timeline, and make a decision that fits real life - not just a spreadsheet fantasy.

Frequently Asked Questions

Should I pay off debt fast or build savings first?

If you have no emergency cushion, doing both at the same time is often the safer move. Paying off debt fast can look good until one surprise expense forces you to use credit again.

Why can an aggressive debt payoff plan fail?

It can fail when it leaves you with no room for real life. A car repair, medical bill, or income dip can wipe out your progress if you have no savings buffer.

Can I still make progress if I split money between debt and savings?

Yes. The debt may take longer to pay off, but a balanced plan can reduce the odds that you will need to borrow again before you finish.

🧱 Ready to Build Your Own Plan?

No loans. No gimmicks. Just a clear way to compare your options and build a debt payoff plan that works in real life.